The assignment problem concerns the allocation of policy instruments to policy targets in order to improve policy effectiveness. Policy instruments are variables or procedures directly controlled by policy authorities, while policy targets are the objectives policymakers seek to achieve, such as full employment, price stability, or external balance. Because different government agencies may control different instruments, determining the correct allocation is critical for effective policymaking.

Trevor Swan (1960) framed the assignment problem in the context of an open economy pursuing two central objectives: internal balance (full employment with price stability) and external balance (a sustainable current account position). External imbalances can spill over across borders, especially when large economies are involved, making efficient policy assignment a matter of international as well as domestic importance.

The Tinbergen Rule

Jan Tinbergen (1952) established a fundamental principle of economic policy design: to achieve n independent policy objectives, a government must have at least n independent policy instruments. Known as the Tinbergen rule, this result implies that a single instrument cannot simultaneously resolve multiple policy problems.

For example, if a country faces both unemployment and a current account deficit but controls only government spending, it can address only one objective at a time. Expansionary spending may reduce unemployment but worsen the external deficit, while contractionary spending improves the balance of payments at the cost of higher unemployment. Introducing a second instrument, such as exchange rate policy, raises the crucial question of correct assignment: which instrument should target which objective?

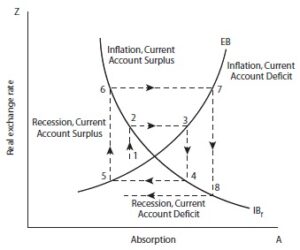

Adjustment in the Swan Diagram

Swan (1960) illustrated the assignment problem using what is now known as the Swan diagram. The diagram plots absorption (domestic demand) on one axis and the real exchange rate on the other. Two schedules define equilibrium conditions: the internal balance schedule (IBf) and the external balance schedule (EB).

The internal balance schedule is downward sloping, reflecting the fact that currency appreciation reduces demand for domestic goods and must be offset by higher government spending to maintain full employment. The external balance schedule is upward sloping because real depreciation improves the current account and must be offset by higher absorption to prevent a surplus.

Incorrect assignment of instruments can lead to divergence from equilibrium. For instance, assigning exchange rate policy to internal balance and government spending to external balance can cause the economy to spiral away from equilibrium through successive adjustments. Reversing the assignment—using government spending for internal balance and the exchange rate for external balance—leads to convergence.

This result depends on the relative slopes of the schedules. The exchange rate has a stronger effect on external balance than on internal balance, while government spending has a stronger effect on internal balance. Correct assignment exploits these relative strengths.

Effective Market Classification

Robert Mundell (1962) formalized the logic of correct assignment as the principle of effective market classification. Each policy instrument should be assigned to the target variable on which it has the greatest relative effect, or comparative advantage.

In a fixed exchange rate system with interest rates and fiscal policy as instruments, if interest rates have a stronger impact on capital flows and external balance, they should be assigned to the balance of payments objective. Fiscal policy, which more directly affects aggregate demand, should be assigned to internal balance.

Misassignment can cause cumulative divergence. For example, using fiscal contraction to correct a current account deficit worsens a recession, while subsequent monetary easing to stimulate output may trigger capital outflows, further destabilizing the external position. Proper assignment avoids this instability.

Allowing for Shocks

The basic assignment framework assumes a deterministic environment without random shocks. Poole (1970) extended the analysis to stochastic settings, focusing on the choice of monetary policy instruments.

If aggregate demand is subject to larger random shocks than money demand, using the money supply as the policy instrument reduces output volatility, as interest rates adjust countercyclically. Conversely, if money demand is more volatile, targeting interest rates stabilizes output by allowing automatic adjustment of the money supply.

Choosing the wrong instrument under uncertainty can amplify fluctuations rather than dampen them. Thus, the assignment problem remains relevant not only for structural policy design but also for managing economic volatility.

Although real-world economies adjust simultaneously rather than sequentially, and markets themselves play an adjustment role, the assignment problem provides a powerful framework for thinking about policy coordination. It is particularly valuable when different instruments are controlled by separate institutions, such as central banks and fiscal authorities.